Energy Market Overview: Warmer March Weather Brought a Significant Drop in Power Prices

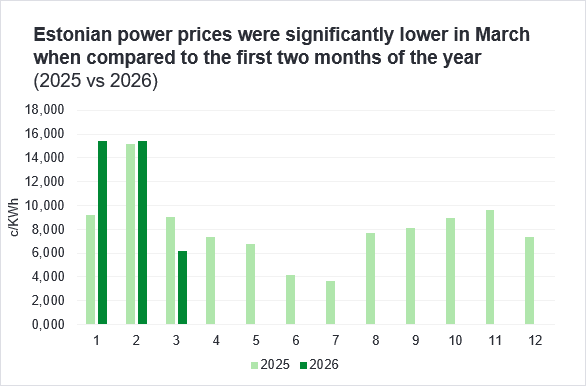

With the cold period coming to an end, consumers in Estonia have been able to enjoy noticeably lower power prices, especially during daytime hours when solar generation in the region has started to increase rapidly. In March, the average power price in Estonia reached 6.1 cents per kilowatt-hour, more than halving compared to the first months of the year, when prices remained slightly above 15 cents per kilowatt‑hour. Compared to March 2025, the price decreased by 32%.

The decline was driven by lower consumption resulting from warmer temperatures, strong import flows from Finland, and a higher share of renewable energy in the overall consumption mix.

A Sharp Drop in Consumption Brought Prices Down

The single biggest driver behind the lower prices was the substantial decline in electricity consumption in both Estonia and the wider Baltic region. While consumption in January and February ranged between 847 and 944 GWh, March consumption in Estonia totalled just 696 GWh – nearly 20% lower than in the previous winter months. Baltic-wide consumption reached 2292 GWh, also roughly 20% lower than in February. Compared to March of last year, total Baltic demand remained at a similar level.

The sharp increase in demand seen at the beginning of the year, followed by a sudden decline, has a very clear effect on the electricity market. It highlights what happens in regional markets when consumption is high but there is not enough affordable local generation available to cover it.

Another important factor pushing prices lower was the growing share of renewable energy in the consumption mix. In March, wind, solar and hydro generation together covered 63% of total Baltic electricity demand, and accounted for as much as 75% of the total generation mix. The higher share of renewables resulted in lower market prices and reduced the need to dispatch more expensive fossil‑fuel‑based power plants.

Warming Weather and Rising Solar Production Point to Continued Price Declines

If warmer weather and sunnier periods continue, and cross‑border interconnections operate as expected, further reductions in power prices can be anticipated—particularly relative to the first months of the year. Several key factors support this outlook.

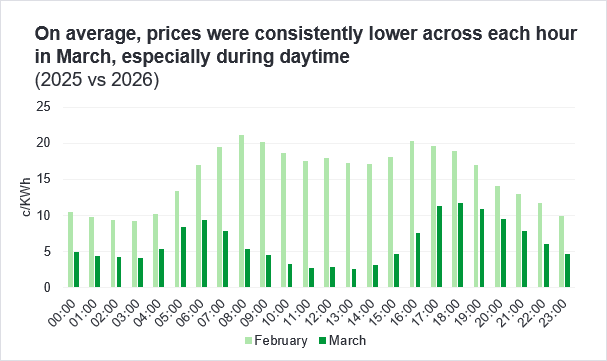

First, as daylight hours increase, solar production across Estonia and the Baltics is rising. This is bringing back the familiar summer pattern of two‑peaked daily prices. During midday hours, when solar generation is plentiful, prices can fall below 1–2 cents per kilowatt‑hour, while during hours without sun, prices are set by more expensive dispatchable assets or imports.

In March, solar production in Estonia reached 105 GWh—more than 5.5 times higher than February’s 19 GWh. Based on historical patterns, this growth is expected to continue through spring and into summer.

Additionally, March brought a significant increase in Latvian hydro production, an extremely important and very cheap source of electricity for the Baltic region. Hydro generation in Latvia grew nearly fourfold, reaching 487 GWh and covering almost 20% of total Baltic electricity demand in March.

Since the Baltic countries operate as a unified electricity system and price region for most of the time, Latvia’s hydro production directly helps push down prices across the entire region.

Imports from Finland Keep Estonian Prices Below the Baltic Average

For the Baltic states, access to cheaper electricity from the Nordic countries remains essential, and in many cases these markets set the price for our region. Most importantly, imports from Finland via the Estlink cables play a major role in lowering prices in Estonia.

Because transmission bottlenecks between Estonia and Latvia persisted in March, a larger share of cheap Finnish electricity remained in Estonia. As a result, Estonia’s average March price was about 20% lower than Latvia’s and roughly 25% lower than Lithuania’s. These internal regional bottlenecks created a situation where excess Finnish electricity accumulated mostly in Estonia, to a smaller extent in Latvia, and only minimally reached Lithuania.

Fossil-Based Generation Declined

As a result of all these factors, fossil‑fuel‑based production in the Baltics fell by nearly 80%, as the market was dominated by renewable sources—primarily solar and hydro—supported by cheaper imports from the Nordic region. Consequently, average peak-hour prices decreased significantly as well.

What to Expect in April?

Similar market dynamics can be expected in April. Solar production will continue to increase, and access to Nordic imports is likely to remain strong, keeping daytime prices low, especially during sunny periods. Nighttime and morning peak prices, however, will depend on several interconnected factors, including local consumption levels, the volume of hydro production, regional wind generation, the availability of dispatchable assets, and the import capacity from the Nordic countries. The conflict in the Middle East is not expected to significantly affect the Baltic power market at this stage, as renewable output remains strong and the share of fossil‑based production is notably lower than during the winter months.

Karl Joosep Randveer, Energy Trading Analyst at Enefit

The market overview has been compiled by Enefit according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Enefit. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Enefit is not liable for any costs or damages that may arise in connection with the use of the information provided.