Energy market overview: Estonia maintained a price advantage over Latvia and Lithuania in May

May brought increasingly summer-like conditions to the Baltic power market. Higher solar irradiation and warmer temperatures reached both Estonia and the wider Baltic region. At the same time, reduced wind and hydropower generation led to greater reliance on dispatchable fossil-fuel plants during certain periods.

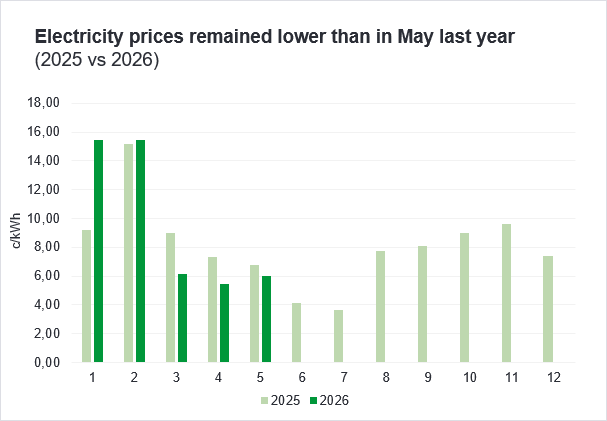

The average power price in Estonia stood at 6.03 c/kWh in May, approximately 11% higher than in April. Compared to May last year, however, the price was still 11% lower.

Notably, Estonia remained significantly cheaper than Latvia and Lithuania. This continues to be driven by constraints on the Estonia–Latvia interconnection, which limit the flow of inexpensive Nordic power – routed through Finland – to the Latvian and Lithuanian markets. As a result, the average price in Latvia and Lithuania reached 8.23 c/kWh in May, nearly 37% higher than in Estonia.

Lower hydro and wind generation increased reliance on fossil capacity

Power prices in the Baltics were primarily shaped by regional renewable generation dynamics. A notable downward impact came from reduced wind output, which increased dependence on fossil generation, particularly as hydropower production declined sharply.

Latvia, the region’s main hydropower producer, saw hydro output fall by close to 50% month-on-month to 223 GWh, supplying significantly less flexible and low-cost renewable energy to the Baltic market. While hydropower covered nearly a quarter of regional demand in April, this share dropped to just 14% in May. The seasonal decline is expected to continue in the coming months.

Wind generation across the Baltics also declined by nearly one-fifth, from 664 GWh in April to 549 GWh in May. Similar to hydropower, the reduction in wind output pushed the region toward more expensive generation alternatives and added upward pressure on prices.

Despite this, renewables still maintained a dominant role. Wind accounted for approximately 27% and solar for 34% of total Baltic consumption, bringing the overall renewable share to around 75% (excluding renewable imports from the Nordics).

In Estonia alone, wind and solar covered approximately 44.4% of domestic demand. It should be noted, however, that this figure excludes imports from Finland and from the rest of the Baltics via Latvia, which would significantly increase the effective renewable share (as reflected in the Baltic-wide numbers).

Solar generation continues to expand across the Baltics

Estonia produced around 164 GWh of solar energy in May, broadly in line with April’s output of 163 GWh. Among the Baltic states, Estonia remained the smallest solar producer, with Latvia generating close to 216 GWh and Lithuania around 320 GWh.

The most rapid growth in solar generation has been seen in Latvia, where output from March to May this year was, on average, approximately 182% higher than during the same period last year. This means that across the key solar months so far (March–May), Latvia has nearly doubled its solar production year-on-year.

This rapid expansion of solar capacity in Latvia is clearly influencing the broader Baltic power market by introducing a significant new source of low-cost energy. Overall, solar generation covered around 34% of total Baltic demand in May – the highest level ever recorded in the region.

June outlook remains dependent on solar and wind availability

Looking ahead, solar generation in June is expected to remain at similar levels to May or decrease slightly, as May has historically been one of the strongest months for solar output. Nevertheless, solar generation should continue to drive a clear intraday price pattern, with higher prices during low solar output periods and lower – or even near-zero – prices during peak generation hours.

As seen in May, the combined effect of declining Latvian hydropower and lower wind output is sufficient to push regional prices higher, particularly during periods when solar generation is limited. During such hours, dispatchable fossil-fuel plants need to be activated to meet demand.

With the heating season now over and overall fossil plant utilisation relatively low, these short-term activations can lead to temporary price spikes above typical spring levels. However, thanks to strong local renewable generation and continued imports of Nordic power via Estonia and Lithuania, such hours are likely to remain limited. As a result, June power prices are expected to stay at least in line with typical spring levels.

Karl Joosep Randveer, Energy Trading Analyst at Enefit

The market overview has been compiled by Enefit according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Enefit. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Enefit is not liable for any costs or damages that may arise in connection with the use of the information provided