Energy Market Overview: Lithuania’s Wind Contribution Influences Baltic Electricity Prices

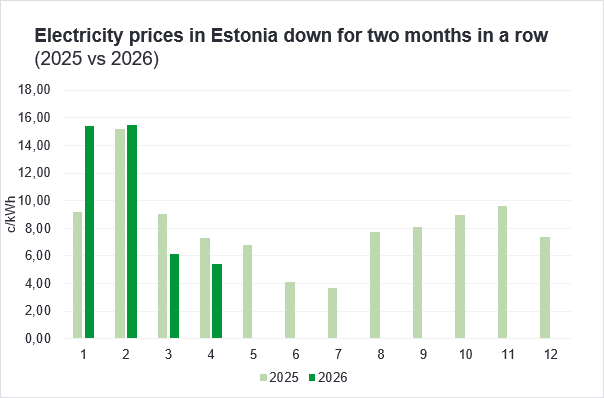

April brought favourable conditions to Estonian consumers and marked the second consecutive month of declining electricity prices. Thanks to sunnier weather and warmer temperatures, the average electricity price in April settled at 5.4 cents per kilowatt-hour, roughly 11.4% lower than in March and more than a quarter lower than in April of the previous year. The last time April was cheaper was in 2021, when the monthly average price stood at 4.4 cents per kilowatt-hour.

The reasons behind the lower prices are clear. Warmer weather reduced heating demand and, as a result, overall electricity consumption. Solar and wind generation increased significantly across the region, bringing a large volume of low-cost electricity to the market. This, in turn, reduced more expensive fossil-based generation. Additional support came from the ongoing Latvian hydropower high season, which helped displace higher-cost fossil-based generation assets.

Comparing Baltic fossil-based electricity production in January and February with April highlights the scale of the shift. In January and February this year, Baltic fossil-based plants produced an average of close to 1,000 GWh per month, whereas in April total fossil-based generation across the region amounted to just 120.5 GWh.

Nearly a third of the electricity consumed in the Baltic region in April came from wind power, close to a fifth from solar, and another fifth from Latvian hydropower. Within the Baltic generation mix, Estonia contributed close to 18% of total regional wind output and slightly over a fifth of total regional solar output. Almost all of the remaining Baltic wind generation came from Lithuania, which accounted for roughly 78% of total wind output. Notably, wind and solar generation together covered as much as 83% of Lithuania’s electricity consumption in April.

The Rollercoaster Pattern in Electricity Prices Is Set to Persist

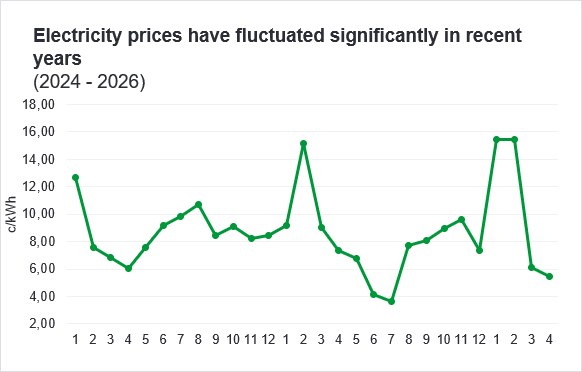

Looking at price developments across Estonia and its neighbouring countries, a familiar rollercoaster pattern emerges. In winter, renewable generation is insufficient to meet higher demand driven by heating needs, and the resulting shortfall must be covered by fossil-based generation, pushing electricity prices up. In summer, generation can at times exceed local demand, driving prices down to levels where electricity is exported. Spring and autumn lie naturally between these two extremes — temperatures are mild and heating demand is lower, yet the combined output from wind and solar has not reached levels that create summer surpluses. As a result, price levels tend to be more moderate and stable.

This pattern illustrates how sensitive the electricity market is to changes in underlying fundamentals. As the Baltic region continues to lack flexible resources — such as battery storage or efficient gas-fired capacity — this seasonal price volatility is expected to persist for some time. At the same time, considering the significant additions of solar capacity in Latvia and Lithuania, electricity prices this summer are likely to match or even fall below last year’s levels across the Baltic region.

May Is Expected to Develop Similarly to April

In May, daytime prices will largely be determined by solar availability. Overnight prices, however, will depend primarily on demand levels, import opportunities from Scandinavia, wind conditions, and Latvian hydropower. In May, hydropower generation typically begins to decline as the spring high-water period comes to an end.

As noted, the rapid expansion of solar generation capacity has now reached all Baltic markets. As a result, a larger volume of low-cost solar electricity — with broader geographic coverage than in previous years — is entering the market, and its impact is likely to be felt more widely across electricity prices throughout the region.

Karl Joosep Randveer, Energy Trading Analyst at Enefit

The market overview has been compiled by Enefit according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Enefit. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Enefit is not liable for any costs or damages that may arise in connection with the use of the information provided.