Energy market overview: Electricity price is increasingly dependent on wind energy and less on solar energy

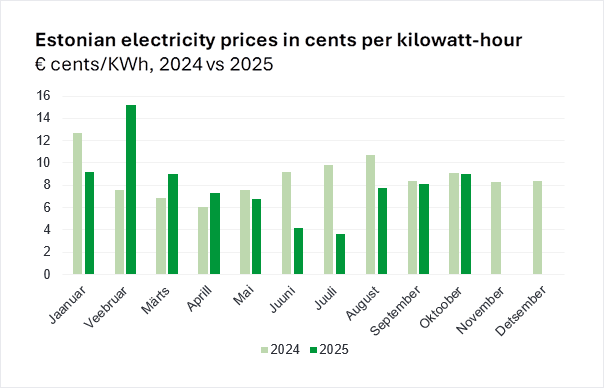

- October prices in Estonia were roughly flat vs last year but about 11% higher than September, mainly because it got colder, solar fell, wind was softer, and the EE–LV link was tighter.

- Bottlenecks kept more cheap Nordic power in Estonia, so Estonia stayed about 15% cheaper than Latvia–Lithuania and relied more on imports (around half of demand, vs ~33% in a typical October).

- Spikes came when wind was low and oil-shale ran high (about 22% of hours): Estonia averaged near 17.3 c/kWh in those hours, and over half of them were ≥15 c/kWh.

- As wintertime steps in during November, prices will continue to depend on import availability from the Nordics—either via NordBalt into Lithuania or Estlink through Estonia—alongside Nordic price levels, wind output in the Baltic region, and, very importantly, temperature.

Seasonal changes, interconnector capacities and production dynamics affected the power prices in Estonia in October

The electricity markets in the Estonian region in October were driven by a mix of production dynamics across the Baltics and interconnection constraints that limited cheap Nordic imports. The price in Estonia averaged at 8.98 c/KWh, almost exactly the same compared to the year before, however near 11% higher compared to September’s 8.11 c/KWh. When compared to the previous month, the key drivers behind the price increase were a continuous decline in the Baltic solar production, the seasonal temperature decrease hitting heating demand higher and a lower-than-usual wind production in Estonia, coupled with less connectivity to Latvia, therefore partly decreasing the inflow of of Lithuanian wind energy produced.

Bottlenecks kept cheap Nordic power in Estonia, but low wind + oil shale drove price surges

As a result of interconnectivity capacities being curbed by close to half between Estonia and Latvia within the entirety of October, Estonian power prices remained near 15% lower than the prices in both Latvia and Lithuania as our southern neighbors did not have as much access to cheaper Finnish electricity through Estlink. This in turn pushed Estonian net imports significantly higher to nearly half of total demand at 48%, clearly higher than the past 5-year October average of 33% - as less imported flows were unavailable for the rest of the Baltics due to interconnection works between Estonia and Latvia, more Finnish imports remained in the Estonian price zone and therefore often helped to keep more expensive gas and oil shale units off the market.

Estonia still experienced a lot of price spikes where the price went over 15 c/kWh. A clear pattern sits behind the spikes: in October, when Estonian oil-shale ran above its usual “on” level (≈186 MW) at the same time as total Baltic wind was below its normal level (≈642 MW), prices increased across the region. In those hours (about 22% of October), Estonia averaged ~17.3 c/kWh and Latvia/Lithuania ~19.5 c/kWh. Across the whole month, 19% of Estonian hours were at or above 15 c/kWh.

Outside this pattern, the region was much calmer: Estonia around 6.6 c/kWh and Latvia/Lithuania around 8.0 c/kWh, and only about one in ten hours above 15 c/kWh. The logic is straightforward: weak wind means the system relies more on oil-shale and other thermal units, which have higher running costs and therefore set the market price more often; with southbound capacity constrained, Latvia and Lithuania also had less access to cheaper Nordic power, so they printed higher prices than Estonia even as Estlink inflows helped soften some peaks in the Estonian zone.

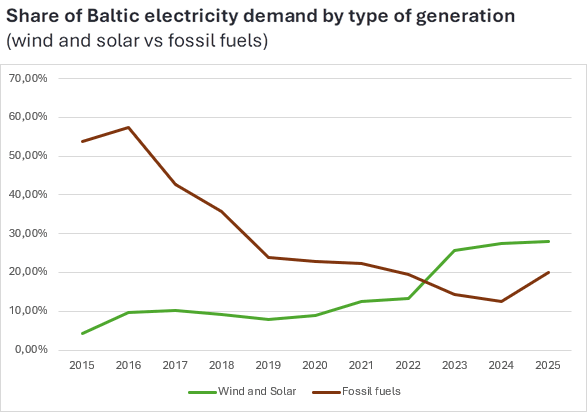

With October, we already see power prices becoming much more dependent on wind energy and less on solar energy

The very low prices seen in summer—often dropping below 10 euros per MWh or even lower—have started to fade. Seasonality is pushing solar out, and Latvian hydroenergy is cooling down for the winter period.

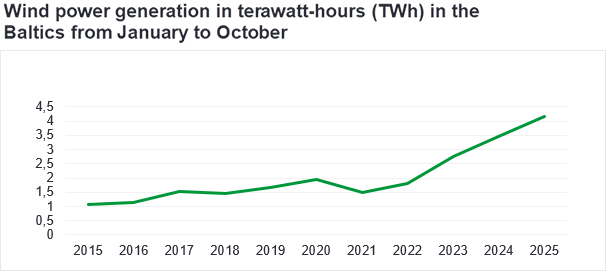

That leaves one consumer-friendly, cheap production asset to pull prices significantly below the high October average price: wind energy. In October, wind alone covered near 12% of total Estonian demand. Compared to last year October’s 20%, it is a large drop, and certainly had an impact on power prices in the Baltic region. At the same time, together with Latvian and Lithuanian wind production, wind power covered near 21% of total Baltic demand – and is expected to increase more towards the winter season arriving. For comparability, if we look at production values from January to October, wind production has grown on average 30% in the past 4 years.

As more wind is added to the mix in Estonia and, more broadly, the Baltic region, dependence on expensive fossil-based assets should decline—gas plants in Lithuania and Latvia or the most expensive market makers, Estonia’s oil-shale plants, which set prices far beyond 15 c/KWh. Another key factor for consumers will remain access to cheap Nordic hydroenergy: as long as mainly Norway, and to a lesser extent the rest of the Nordics, keep producing consistent, predictable hydroenergy, Nordic supply will help pull Baltic power prices down thanks to its relatively low production cost.

November will most probably bring colder weather, deepening the ongoing heating season demand

As days get shorter and colder, Estonian demand typically rises for heating. That brings a pattern seen in previous winters—strictly higher prices during morning and evening peak hours, and relatively lower prices during daytime and night hours.

Last year’s November showed that morning prices between 07.00–09.00 were on average near a 50% higher than the monthly average price. In the most expensive evening hours, 16.00–18.00, prices were on average near 65% higher than the monthly average price. For everyday consumers, it is worth following intraday prices closely—or, depending on needs, considering a fixed price to protect against these strong price fluctuations.

As wintertime steps in during November, prices will continue to depend on import availability from the Nordics—either via NordBalt into Lithuania or Estlink through Estonia—alongside Nordic price levels, wind output in the Baltic region, and, very importantly, temperature. As of now, transmission constraints of close to 50% between Estonia and Latvia are expected to continue in November, therefore restricting cheap Finnish electricity access outside of the Estonian market.

Karl Joosep Randveer, Energy Trading Analyst at Eesti Energia

The market overview has been compiled by Eesti Energia according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Eesti Energia. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Eesti Energia is not liable for any costs or damages that may arise in connection with the use of the information provided.